A flexible ag line of credit can give your farm the steady cash flow it needs, from planting all the way through harvest, in the following ways.

- Captures Early Discounts: Setting up your loan early lets you buy seed and fertilizer during specific times of the year when prices are lower.

- Handles Unexpected Repairs: The line acts as a safety net, giving you quick access to cash if you need to replant crops or repair a broken tractor.

- Gives You Time To Sell: Instead of forcing you to sell grain when prices are low, local bankers can help extend your loan so you can wait for better market conditions.

Every spring, farmers across Iowa and Nebraska prepare to get back into the fields. While upfront costs for fertilizer, fuel, seed and land rent represent a significant investment, managing these expenses can be smooth and stress-free with the right financial strategy in place.

For many producers, a flexible agricultural line of credit acts as a powerful business tool. It funds initial planting costs while providing the flexibility to help handle mid-season surprises like equipment breakdowns, increasing fuel prices or the need to replant a damaged field.

Get started with the following steps to secure your spring planting and support your farm throughout the year with an ag line of credit.

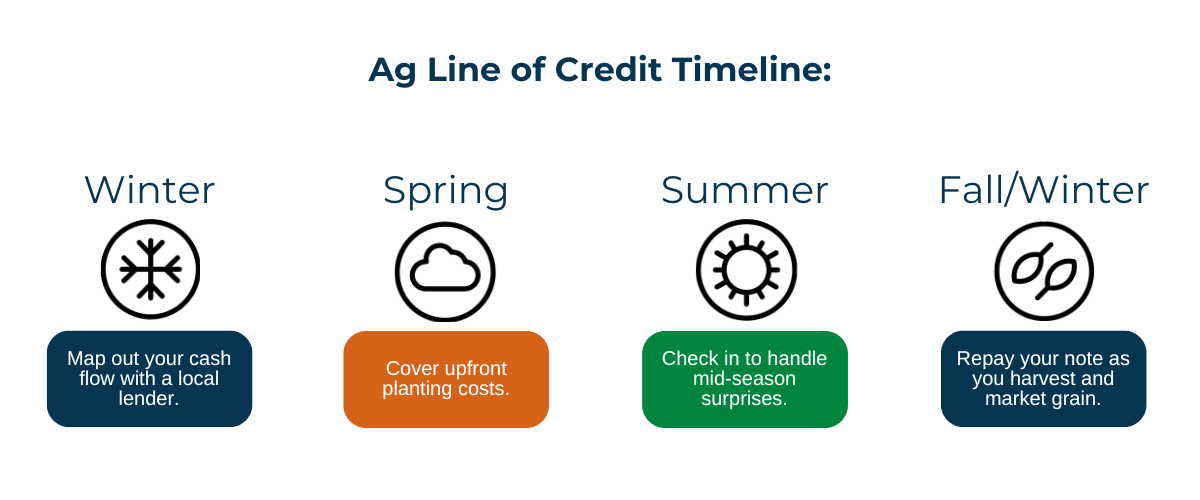

Sit Down and Map Out Your Farm's Cash Flow

The process begins before your tractors hit the field. It is a collaborative effort between you and your banker and is focused on your specific operation. Local ag lenders don’t use rigid, one-size-fits-all formulas or strict per-acre dollar limits. Instead, they sit down with you to review your corn and bean acres, what you own and what you owe.

To build this plan, you and your lender will look at two essential pieces:

- Agriculture Balance Sheet: A financial snapshot that lists your assets (such as land, machinery and stored grain) versus your liabilities (such as land notes or equipment debt).

- Farm Cash Flow Projection: The flow of money moving in and out of your business every month, to ensure that you maintain a positive cash flow.

By combining your agriculture balance sheet with a forward-looking cash flow plan, your lender can build a customized operating line. This matches your credit limit with the needs of your farm. It gives you the funds to cover planting expenses — including seed, chemicals, cash rent and crop insurance premiums — without overextending your business.

Time Your Loan Setup To Capture Early Discounts

A typical farm operating loan is set up as a revolving line of credit that lasts for one year. While many lines are finalized in January, February or March, it is often best to start this conversation with your banker at the end of the prior year.

Locking in these input prices in the late fall or early winter allows you to take advantage of significant order discounts from seed, fertilizer and chemical companies. It is often cheaper than paying full price in the spring, which helps keep your planting costs lower.

Secure the Line With Collateral and Crop Insurance

Once you have input costs locked into your cash flow, the next step is to put the right protections in place. When securing an operating line, community banks rely on your growing crop as the primary collateral. To fully back the loan, lenders will also look at other assets, such as your farm equipment, stored grain or land.

Crop insurance including revenue protection can act as a safety net for producers to protect them from inclement weather, low yields and volatile markets.

Keep in Touch Throughout the Year

Farming moves fast after planting — markets fluctuate and unexpected expenses can pop up. You can protect your momentum and stay ahead of these changes through quick, regular updates with your ag lender.

For instance, if there is a major flood or a late freeze that requires you to replant, your line of credit is designed to quickly adapt. Because your crop insurance policy will usually cover the bulk of the replanting costs, your operating line can immediately be tapped to cover the upfront seed expenses.

Similarly, if a tractor engine or combine breaks down in the middle of harvest, your operating line is built to handle these sudden repair bills. With a revolving line of credit, any money you have paid back from previous crop sales can become available to use again for emergency expenses without requiring a new loan application.

When these moments happen, you can work directly with your lender to run the numbers on your options. Together, you can analyze whether it is more cost-effective to draw from your operating line for repairs or if it is the right time to transition into long-term ag equipment loans or specialized ag equipment financing to upgrade the machine.

Align Repayment With Your Marketing Plan

A standard operating line is timed to match your season: planting, harvesting and selling. Local bankers know you likely won’t sell your grain right away. Instead, you might store it in bins and sell it when prices are favorable.

A one-year loan gives you plenty of time to navigate the market. If you want to hold your grain into the next year for a higher price, a banker can easily transition your remaining loan balance into a separate short-term note backed by that stored grain. This flexibility means you don’t have to force a sale.

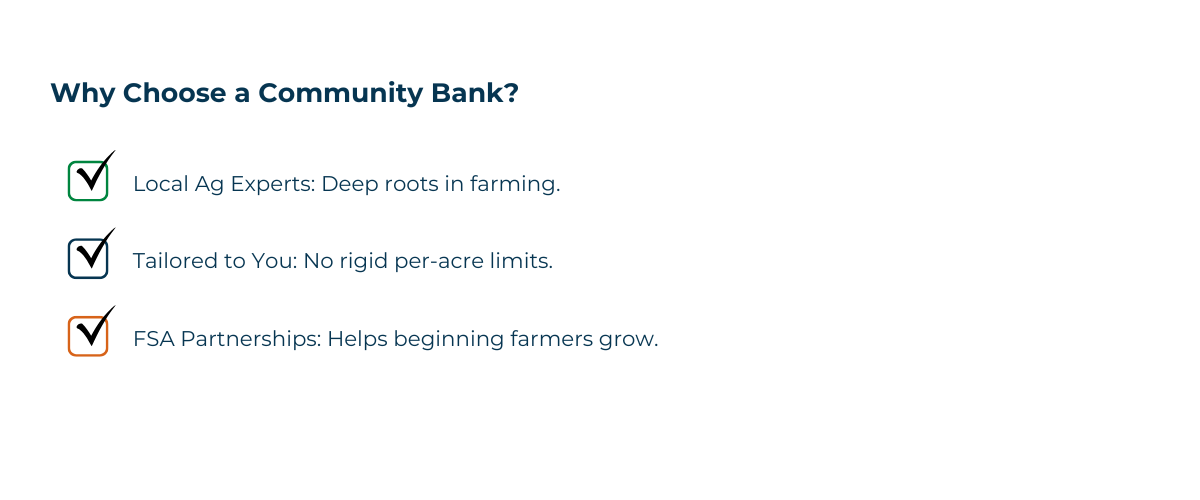

The Community Bank Advantage

When choosing a financial partner to cover planting costs, many producers evaluate the differences between national lenders and local community banks. Agricultural lenders at community banks like Northwest Bank have deep roots in farming. Many grew up on family farms, still farm today or hold agronomy degrees. They understand soil, weather and market conditions.

Rather than keeping the conversation confined to an office, local lenders make it a priority to visit you at your property. Together on the farm, you can build a quick mini-cash flow analysis and talk through how your seasonal numbers are tracking. If you notice in July that a lack of rain is going to hurt your yields, or that grain prices are dropping, you can collaborate on a proactive solution.

Beyond managing seasonal shifts, community banks work with programs that support the next generation of farmers. Community banks partner directly with local Farm Service Agency (FSA) offices. This partnership allows lenders to build specialized operating lines and ag loans with incentives designed specifically for young and beginning farmers.

At the end of the day, using a line of credit successfully comes down to communication. Contact our Agriculture bankers today to learn more about an ag line of credit to help protect your cash flow and keep your farm running strong from planting all the way through harvest.