One of the most complicated aspects of owning a small business is handling taxes. In fact, out of the top 10 most burdensome problems small business owners report, four are tax-related. Managing your taxes doesn’t have to cause you a headache. There are tax advisors and financial resources that can help you save money and make the business tax filling process easier.

If you are filing your business taxes for the first time, or need a refresher, these tax tips for small business can give you a better understanding this season. This article is a general discussion of tax tips and is not intended to be tax or legal advice. Discuss your situation with a tax professional before you prepare your business taxes.

1. Adhere to Federal, State and Payroll Tax Filing Requirements

As a small business owner, you’ll need to pay federal and state income taxes. Federal income taxes go to the federal government to pay for roads, bridges, schools and other resources offered to the general public. Most small businesses don't pay income tax at a business rate, because 75% of small businesses are not C-corporations. They are considered pass-through entities, which means you’ll likely pay taxes at current individual income tax rates.

If your business has employees, you’ll be responsible for paying state employment taxes. These vary by state, but often include workers’ compensation insurance, unemployment insurance taxes and temporary disability insurance. You might also be responsible for withholding employee income tax. Check with your state tax authority to find out how much you need to withhold and when you need to send it to the state. State income tax laws are determined by location and business structure, so you’ll need to check with state and local governments to know your business’s tax obligations.

You'll also need to pay attention to the federal payroll tax, which funds such government assistance programs as Medicare, Social Security and federal unemployment. In most cases, you and your employees share this tax liability. The tax is based on wages paid, with the business covering 7.65% and your employee 7.65%. If you are self-employed, your net self-employment income may be subject to the full 15.3% tax rate. Your total cost in payroll taxes largely depends on how many employees you have, how much you pay them and where you employ them.

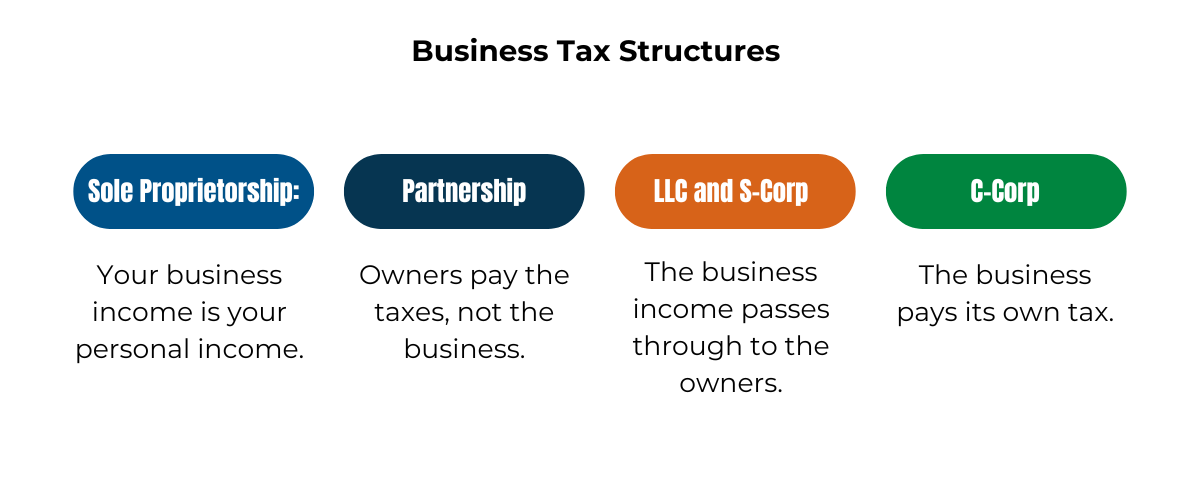

2. Understand That Tax Rules Differ Based on Business Structure

The structure of your small business has financial and tax implications. Your business likely falls into one of four categories: sole proprietorship, partnership, limited liability company or a C or S corporation. The business structure determines your small business tax filing obligations. Sole Proprietorship

Sole Proprietorship

A sole proprietorship consists of a single owner who does not file a separate tax return for their business. They are responsible for paying income tax and a 15.3% self-employment tax. The self-employment tax is equal to the amount they would typically withhold and match for FICA, Medicare and Social Security.

Partnership

A partnership is a lot like a sole proprietorship but consists of two or more business partners. A partnership files an annual information return to report income, deductions, gains and losses, but does not pay income tax as a business.

Limited Liability Company (LLC)

An LLC is a business structure with one or more members (owners). Many states do not restrict membership, meaning that any individual, other company, foreign entity or even another LLC can be a member of your LLC. A single-member LLC is taxed as a sole proprietor by default. A multi-member LLC is taxed as a partnership by default. This means that the business itself does not pay taxes. Instead, the owner and the other members will pay taxes on their respective portions of the profits when they file personal tax returns. This can help lower the tax burden if the business takes a loss in a particular year.

C or S Corporation

A corporation is a type of business entity created by filing articles of incorporation with the state. A corporation’s owners are known as shareholders, and a corporation also has officers and directors who run the business.

C corporations vs S corporations: C corporations are typically capital-intensive businesses. Publicly traded corporations are required by law to be structured as C corporations. The C-corp is a separate legal entity that pays a flat federal tax of 21% on all its profits. An S corporation does not have its own tax rate structure. Income from an S-corp is taxed based on each shareholder’s personal return according to their ownership percentage. C corporations and S corporations are taxed differently, although neither structure pays self-employment tax on its profits.

3. Look Into Bonus Depreciation or Section 179

Bonus depreciation and Section 179 are both options that allow you to deduct the cost of fixed asset purchases instead of depreciating them over a period of years. Bonus depreciation allows for the depreciation on used equipment; although it must be “first use” by the purchasing business and there are no write-off limits. According to the One Big Beautiful Bill Act (OBBBA), there is a permanent 100% bonus depreciation for most property acquired after Jan. 19, 2025. However, it’s important to stay up to date on current regulations.

Section 179 allows you to deduct the cost of certain property, including equipment and personal property, as an expense when it’s placed in service. There are rules around how Section 179 can be claimed. The property must be used for business purposes more than 50% of the time, actively used in the current financial year and purchased outright. There’s also a limit on the amount you can write off.

4. Apply for the Qualified Business Income (QBI) Deduction

The Tax Cuts and Jobs Act introduced a significant change that affects certain small businesses called a qualified business income (QBI) deduction, otherwise known as Section 199A deduction. The QBI deduction trims eligible taxable income by 20% if you are a sole proprietor, LLC, partnership or S corporation. It isn’t available for C corporations, and there are specific limits and detailed calculations involved. Your tax professional can calculate this deduction for you.

5. Set Up a Retirement Account

Business owners can get a legal tax break by contributing some of their business’s profits to a retirement account. If you don’t have a retirement plan, there are several options, including individual 401(k), Simplified Employee Pension (SEP) IRA and Savings Incentive Match Plan for Employees (SIMPLE) IRA. Here’s a quick breakdown of each:

- Individual 401(k): A popular option to build up your retirement account quickly if you have a lot of money to contribute.

- SEP IRA: Ideal for sole proprietors since account fees are low and any contributions you make are tax deductible.

- SIMPLE IRA: A good plan if you’re running your own business and looking to expand. You can keep investing with this type of an account even after you’ve hired an employee. But you have to match your employee’s contributions up to a certain amount.

Your business may also decide to contribute to your employees’ retirement plan. Any contributions made are tax deductible. By setting up retirement plans, you can create tax savings and prepare for you and your employees’ financial future at the same time.

6. Deduct Vehicle Expenses and Mileage

Some mileage on a personal car that is leased or owned and used for business is tax deductible. The simplest method for calculating the deductible amount is multiplying the number of business miles driven by the IRS mileage rate, which changes each year. However, your daily commute is not deductible. The IRS views the commute between home and work as a personal trip.

Another option is to deduct the cost of the vehicle and the expenses related to maintaining the vehicle (repairs, fuel, etc.) This option cannot be used in the same year that you take the mileage deduction stated above.

Every business’s tax situation is unique, so it’s important to work with a tax professional and a certified public accountant (CPA) to handle your small business taxes. They stay well-informed about current tax laws and regulations, so you don’t have to worry about missing critical details or deadlines.

Reach out to a tax expert today to learn more about financial planning and tax preparation tips.