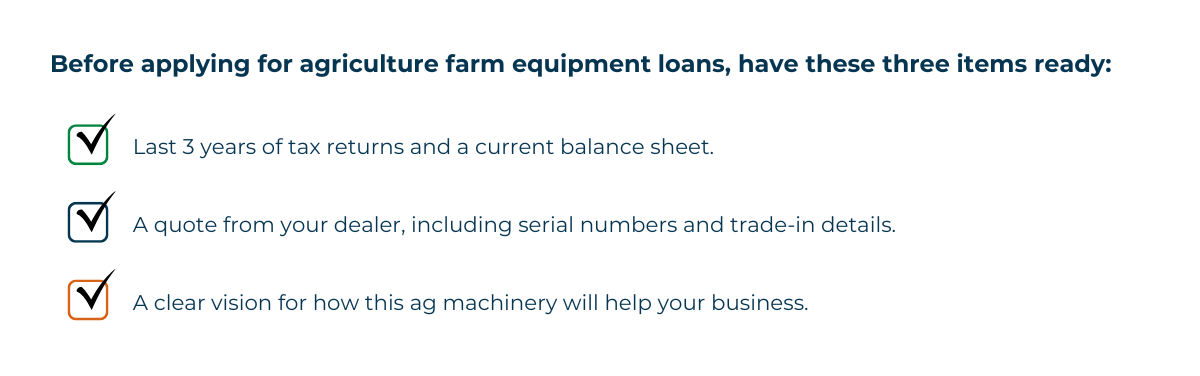

As a producer, your success depends on reliable ag machinery. Whether you are looking for tractor financing or specialized agriculture farm equipment loans, choosing the right partner is critical. Because you rely so heavily on your tools, you need to look beyond the price tag when determining whether a farm equipment loan is the best financing option. When you are making an initial investment or replacing a piece of heavy equipment, you must consider how that debt fits into your long-term operation.

If you’re considering loans for farm equipment for a new or used purchase, ask yourself these questions.

What is my farm’s current financial position?

Before signing any paperwork, pull out your current budget and let it serve as a financial roadmap to help guide your purchase decision. High-quality machinery is a large investment, and it is rare for an operation to purchase multiple pieces of heavy equipment in a single year. Typically, the budget encompasses everything from crop yields and livestock prices to production expenses, such as fertilizer, fuel, insurance and rent.

As you look at your budget, ask yourself, “If I can only buy one thing right now, and I can’t make another purchase for the next three to five years, what should I buy?” This level of financial insight is beneficial when you sit down with your banker to compare ag equipment loans.

Your banker will help you compare your total cost of ownership for the new equipment compared with the equipment you want to trade in. They will also work with you to explore agricultural financing options based on the type of business you own. For example, the terms for financing a tractor can differ significantly for a livestock farmer and a cash grain operation.

Even if you have had financial hurdles in the past, don't assume financing is out of reach. Your banker can discuss specialized options and explain how to finance a tractor by leveraging collateral or flexible repayment schedules.

What is the financial impact on my business?

Every large purchase requires a close look at your debt. The goal is to make sure the new machinery pays for itself by helping you work faster or avoiding expensive breakdowns.

The best way to judge this is by looking at how the purchase affects the overall debt and cash flow of your business. Even if you can afford the specific monthly payment for a new tractor, you need to be sure your business as a whole still has the cash flow it needs for seeds, fuel and emergencies. If the new equipment doesn’t support the overall financial health of your farm, it might be better to defer the purchase.

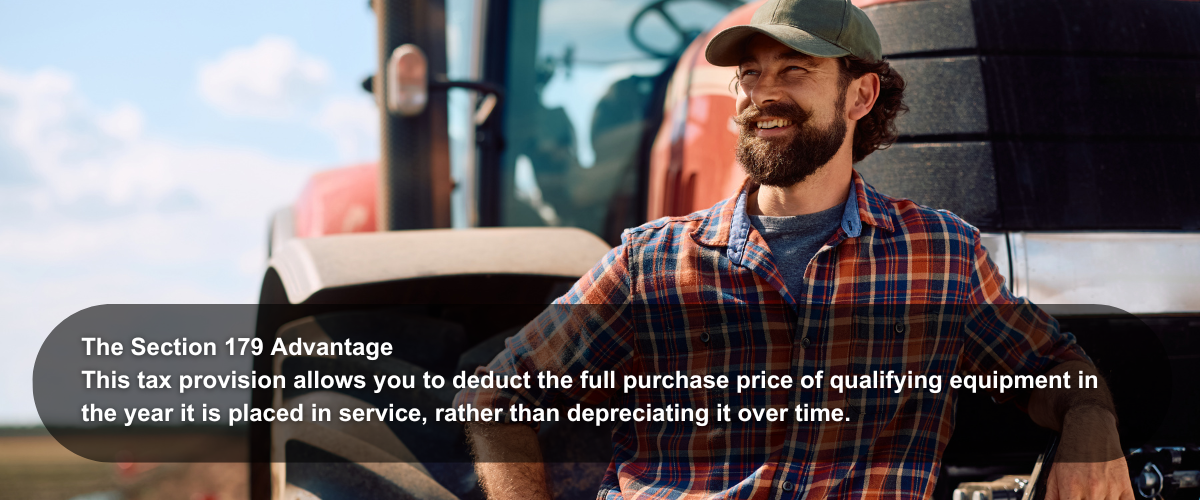

Beyond your monthly loan payments, you should also look at the tax savings that come with farm machinery financing. To get the most out of your investment, it helps to understand section 179.

The section 179 deduction is a rule that lets you deduct the full price of your equipment from your taxes right away. Usually, you would have to spread that deduction out over many years. By using section 179, you can lower your tax bill significantly in the first year. This keeps more cash in your pocket to help pay for the equipment or other farm expenses.

To use this benefit, you must follow the “Placed in Service” rule, meaning the equipment must be on your farm and ready to work during the same tax year you plan to claim the deduction. Just ordering a machine or signing a contract isn't enough; it has to be on-site and ready for use to count for that tax year.

Should I choose a loan or a lease?

One of the most common questions is whether a farm equipment loan is better than a lease. The answer depends on your long-term goals:

- Choose a loan if: You want to own the asset outright, build equity and keep the equipment for its entire working life. This path often costs the least over the long term.

- Choose a lease if: You want a lower monthly payment to keep your cash flow flexible or if you prefer to upgrade to the latest technology every few years without the hassle of selling a used machine.

What is the long-term value?

When buying ag machinery, think about how well it holds its value. Choosing equipment with a strong reputation and a solid dealer network ensures that when you are ready to upgrade again, your trade-in value will be as high as possible. Additionally, consider the cost of maintenance. Sometimes a slightly higher monthly payment on a newer machine is cheaper than the constant repair bills and downtime costs of an older, used machine.

Who should be involved in the decision?

You shouldn’t have to make these decisions alone. Having a team of people you know and respect to serve as a sounding board is a huge asset for your business. It is much easier to reach your goals and avoid financial stress when you work with your banker and CPA as a team. Here’s why their help is so valuable:

- Your banker: They help you look closely at your finances to see what you can afford. They will also walk you through different options — like leasing versus buying — to find the best fit for your specific farm.

- Your CPA: Your tax professional plays a vital role in making sure the purchase actually saves you money. They understand the complex tax rules, like bonus depreciation, and can give you advice on whether a purchase is the right move for your bottom line.

If you are exploring an equipment purchase for your business, contact one of our business bank representatives today to learn more about the support and resources Northwest Bank can offer your business.